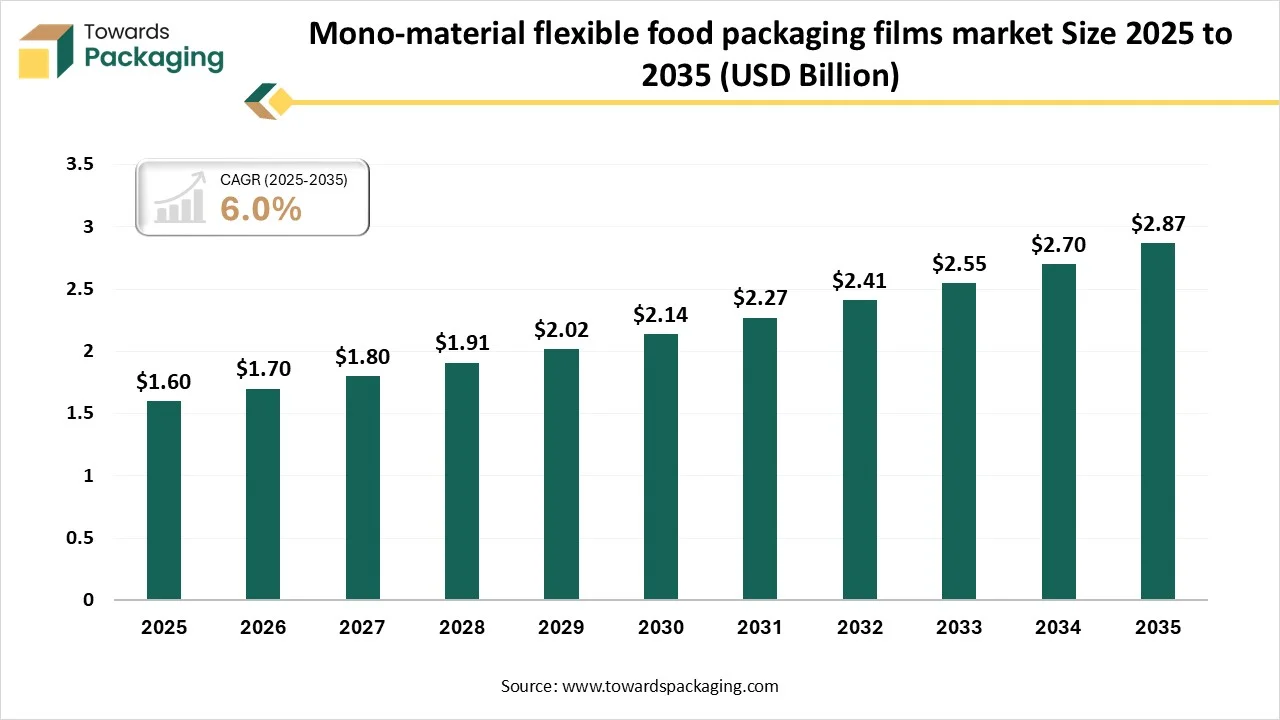

Ottawa, March 04, 2026 (GLOBE NEWSWIRE) — The global mono-material flexible food packaging films market size stood at USD 1.6 billion in 2025 and is projected to reach USD 2.87 billion by 2035, according to a study published by Towards Packaging, a sister firm of Precedence Research. Request Research Report Built Around Your Goals: sales@towardspackaging.com The market is expanding due to rising demand for recyclable, single-material solutions that simplify waste management. Growing focus on sustainability, regulatory pressure, and consumer preference for eco-friendly packaging is driving innovation in durable, lightweight, and high-barrier films. Why is the Mono-Material Flexible Food Packaging Market Gaining Strategic Importance? Mono-material flexible food packaging refers to packaging films made from a single type of polymer, enabling easier recycling and reduced environmental impact compared to multi-layer laminates. The market is gaining strategic importance as manufacturers, retailers, and regulators prioritize sustainable packaging solutions. Its eco-friendly nature, combined with barrier performance, lightweight properties, and compatibility with existing production lines, makes mono-material films critical for reducing plastic waste and meeting growing consumer and regulatory sustainability demands. Private Industry Investments for Mono-material Flexible Food Packaging Films: What Are the Latest Key Trends in the Mono-material Flexible Food Packaging Films Market? Shift Toward Fully Recyclable Structures Brands are increasingly replacing multi-layer laminates with mono-material films that use a single polymer type, such as polypropylene (PP) or polyethylene (PE). This simplifies recycling streams, improves end-of-life processing, and aligns with extended producer responsibility (EPR) mandates, meeting stakeholder demands for more sustainable packaging without sacrificing barrier performance. Enhanced Barrier and Functional Properties Innovations in coating technologies and polymer modifications are enabling mono-material films to match the oxygen, moisture, and light barriers previously achievable only with multi-layer structures. These advancements support longer food shelf life and broader application in snacks, frozen foods, and fresh produce, reducing waste while maintaining product quality. Integration with Smart Packaging Technologies Mono-material films are increasingly being engineered to support smart packaging features such as freshness indicators, QR codes, and temperature sensors. Because these films are compatible with digital printing and sensor integration, brands can enhance traceability, consumer engagement, and real-time quality monitoring without complicating recycling. Use of Bio-based and Recycled Polymers Manufacturers are incorporating bio-based polymers (e.g., bio-PE) and post-consumer recycled content into mono-material films to reduce reliance on virgin fossil resources. This trend not only improves sustainability credentials but also helps companies meet regulatory targets for recycled content and circularity commitments. Lightweighting and Material Optimization Efforts to reduce material use through downgauging and structural redesign are gaining traction. By optimizing film thickness and strength, companies are cutting resource use and transport emissions, while maintaining functional performance, ultimately lowering cost and environmental footprint What is the Potential Growth Rate of the Mono-material Flexible Food Packaging Films Industry? The mono-material flexible food packaging films industry is poised for rapid expansion as sustainability mandates, recycling infrastructure investments, and consumer demand for eco-friendly packaging accelerate. Regulatory pressure to reduce plastic waste, coupled with innovation in high-performance mono-material solutions that rival traditional multi-layer films, is driving broad adoption across food categories. Increased corporate commitments to circularity and rising implementation in regions with advanced recycling systems further support strong long-term growth prospects globally. Get All the Details in Our Solutions – Access Report Sample: https://www.towardspackaging.com/download-sample/5967 Regional Analysis: Who is the leader in the Mono-Material Flexible Food Packaging Films Market? Europe dominates the market due to strict regulatory frameworks promoting recyclability and circular economy initiatives, such as the EU Plastics Strategy. Advanced recycling infrastructure, widespread adoption of extended producer responsibility (EPR) schemes, and strong consumer preference for sustainable packaging drive demand. Additionally, leading food and packaging manufacturers in Germany, France, and the Netherlands are actively transitioning to mono-material solutions, reinforcing Europe's strategic leadership in eco-friendly packaging innovation. UK Mono-Material Flexible Food Packaging Films Market Trends In the UK, the market is shaped by strong regulatory and retail sustainability pressures, especially from the UK Plastics Pact, Extended Producer Responsibility schemes, and the Plastic Packaging Tax, which financially rewards recyclable mono-material formats and penalizes complex laminates. Retailers and converters are adopting high-barrier PE/PP films and recyclable structures across food, chilled, and pet food segments, while leading manufacturers like Coveris win awards for mono-material innovations and expand domestic recyclable-film production hubs to support circularity and performance requirements. Asia Pacific's Growing Mono-Material Flexible Food Packaging Films Industry The Asia-Pacific region is expected to be the fastest-growing region in the market due to rapid urbanization, rising disposable incomes, and growing awareness of sustainable packaging solutions. Expansion of modern retail and e-commerce channels, coupled with increasing demand from the food and beverage sector, is accelerating adoption. Additionally, government initiatives promoting recyclable packaging and investments in local production capacity make the region highly opportunistic for mono-material film manufacturers. China Mono-material Flexible Food Packaging Films Market Trends In China, the market is driven by the rapid adoption of recyclable PE and PP structures across snacks, fresh produce, and e-commerce food segments. Local converters are investing in high-barrier mono-material solutions to meet tightening national policies on plastic waste and recycling. Retailers and brand owners increasingly favor designs that simplify sorting and end-of-life processing, while domestic recyclers scale infrastructure, making China a key growth hub for sustainable flexible packaging. More Insights of Towards Packaging: Segment Outlook Material Type Insights The polyethylene (PE) mono-films segment dominates the mono-material flexible food packaging films market due to its excellent recyclability, cost-effectiveness, and versatile barrier properties. PE films offer strong moisture resistance, durability, and compatibility with printing and sealing processes, making them ideal for snacks, frozen foods, and e-commerce packaging, while supporting sustainable, single-polymer recycling initiatives. The polypropylene (PP) mono-films segment is expected to be the fastest-growing in the market due to its superior heat resistance, clarity, and strength, making it suitable for high-temperature packaging, microwaveable meals, and sterilized products. Its lightweight, durable, and recyclable nature supports sustainability goals, while technological advancements in barrier coatings enhance oxygen and moisture protection. The growing demand from the food and beverage sector further accelerates PP monofilm adoption globally. Film Structure Insights The multi-layer mono structures segment dominates the mono-material flexible food packaging films market due to its ability to combine multiple functional layers using a single polymer type, providing excellent barrier, mechanical, and sealing properties. This structure ensures product protection, extended shelf life, and recyclability, making it ideal for snacks, frozen foods, and ready-to-eat meals, while meeting sustainability and regulatory requirements. The single-layer mono-films segment is expected to be the fastest-growing segment in the market due to its simplicity, cost-efficiency, and ease of recycling. Its lightweight yet durable structure suits snacks, fresh produce, and e-commerce packaging, while enhanced clarity, sealability, and printing compatibility enable versatile applications. These features align with sustainability goals, supporting rapid adoption across diverse food and beverage sectors. Packaging Format Type Insights The pouches (stand-up, flat, zipper) segment is the dominant segment in the mono-material flexible food packaging films market due to its convenience, versatility, and strong barrier properties. These formats offer resealability, shelf stability, and superior product visibility, making them ideal for snacks, pet food, and powdered products. Their compatibility with mono-material films supports recycling and sustainability initiatives while meeting consumer demand for easy-to-use, high-quality packaging that preserves freshness. The vacuum & modified atmosphere packaging (MAP) films segment is expected to be the fastest-growing in the market due to its ability to extend shelf life, preserve freshness, and maintain product quality. These films provide strong oxygen and moisture barriers, are compatible with recyclable mono-material structures, and are increasingly adopted for meat, seafood, and ready-to-eat meals, aligning with sustainability and consumer convenience trends. Food Category / Application Insights The snacks & confectionery segment is the dominant segment in the mono-material flexible food packaging films market due to high consumer demand for convenient, ready-to-eat products. Mono-material films provide excellent barrier properties, protecting flavors, texture, and freshness, while enabling attractive packaging designs like stand-up pouches and flow wraps. Their lightweight, durable, and recyclable nature aligns with sustainability goals, making them the preferred choice for large-scale snack and confectionery manufacturers. The frozen & refrigerated foods segment is expected to be the fastest-growing segment in the market due to increasing demand for convenient, ready-to-eat meals and perishable food preservation. Mono-material films offer excellent moisture and oxygen barriers, heat-sealability, and durability under freezing conditions. These features maintain product quality, extend shelf life, and support sustainable recycling initiatives, driving rapid adoption in frozen meals, chilled ready-to-eat foods, and dairy product packaging. Recent Breakthroughs in the Mono-material Flexible Food Packaging Films Industry Top Companies in the Global Mono-material Flexible Food Packaging Films Market Segment Covered in the Report By Material Type By Film Structure By Packaging Format By Food Category / Application By Region North America: South America: Europe: Eastern Europe Asia Pacific: MEA: Invest in Our Premium Strategic Solution: https://www.towardspackaging.com/checkout/5967 Request Research Report Built Around Your Goals: sales@towardspackaging.com About Us Towards Packaging is a global consulting and market intelligence firm specializing in strategic research across key packaging segments including sustainable, flexible, smart, biodegradable, and recycled packaging. We empower businesses with actionable insights, trend analysis, and data-driven strategies. Our experienced consultants use advanced research methodologies to help companies of all sizes navigate market shifts, identify growth opportunities, and stay competitive in the global packaging industry. Stay Connected with Towards Packaging: Our Trusted Data Partners Precedence Research | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Healthcare Webwire | Packaging Webwire | Precedence Research Insights Towards Packaging Releases Its Latest Insight – Check It Out: Sustainable Aerosol Packaging Market Size, Trends and Segments (2026-2035) Poly-Woven Packaging Market Size, Trends and Segments (2026-2035) Mono-Material Cosmetic Tubes Market Growth, Trends & Forecast (2025-2035) U.S. Beer Packaging Market Size and Trend, Segment Outlook (2026-2035) Cold Chain Packaging Refrigerants Market Size, Trends and Segments (2026-2035) Packaging Adhesive Market Size, Trends and Regional Analysis (2026-2035) Heavy-Duty Corrugated Bulk Boxes Market Size and Segments Outlook (2026-2035) Next-Gen Paper & Fiber-Based Packaging Market Size, Trends and Regional Analysis (2026-2035) Flow Wrap Packaging Market Size, Trends and Competitive Landscape (2026-2035) India Molded Pulp Packaging Market Size, Trends and Segments (2026-2035) Polyethylene Films Market Size, Trends and Volume (2026-2035) Thin Wall Packaging Market Size and Segments Outlook (2026-2035) Dunnage Packaging Market Size, Trends and Segments (2026-2035) Liquid Packaging Market Size and Segments Outlook (2026-2035) Food Packaging Market Size, Trends and Segments (2026-2035) U.S. Seed Packaging Market Size and Segments Outlook (2026-2035) Europe Pharmaceutical Glass Packaging Market Size, Trends and Segments (2026-2035) Uncoated Paperboard For Luxury Packaging Market Size and Segments Outlook (2026-2035) Consumer Packaged Goods (CPG) Market Size, Trends and Competitive Landscape (2026-2035)

Pinterest | Medium | Tumblr | Hashnode | Bloglovin | LinkedIn – Packaging Web Wire | Globbook | Substack | Bluesky | Justdial | Crunchbase | TrustPilot | Bizcommunity

![]()